HomeEquity release relevant for high net worth clients

Blogs

Why equity release is increasingly relevant for high net worth clients

Years of solid house price growth in the UK has left many individuals and couples with a very large sum of money locked in their homes. Equity release is, of course, one way of unlocking this accumulated wealth without the substantial disruption of leaving a much loved home.

However, equity release is often seen through a narrow lens of financial distress, an option of last resort where clients cannot make ends meet. In contrast, particularly in today’s low interest rate environment, IFAs should see equity release as a practical financial planning tool, even where a client is wealthy. Let’s take a look.

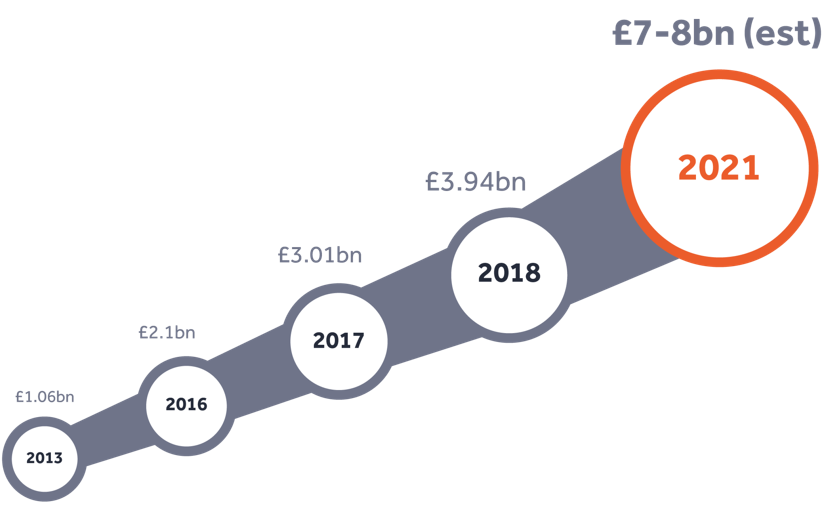

The equity release market is growing rapidly

UK house prices have had a long period of solid growth over the past 20 years, allowing home owners to benefit from large rises in the valuations of their homes, meaning mortgage-free over 55s are potentially sitting on large amounts of equity tied up in their home.

In turn, the amount of money lent through equity release plans is rising fast. With £1.06bn lent in 20131, the total amount released, based on previous growth, is on course to reach around £7-8bn by 2021.

Equity release could benefit high net worth clients too

Indeed, an IFA’s high net worth clients in particular stand to gain substantially from harnessing the equity in their homes. With the large sums available IFAs should consider these four scenarios when dealing with a wealthy client that owns property:

Equity release could enhance the lifestyle of a wealthy client

It is not uncommon for people over 55 to be asset-rich, but relatively cash poor. Where clients are making ends meet without truly enjoying their wealth, IFAs can recommend equity release as an option to help boost a client’s lifestyle without the disruption of selling up and downsizing.

A more flexible approach to retirement income

With the advent of pension freedoms, clients now have more flexibility over how and when they access the cash in their pension funds. Using housing wealth to complement a retirement income strategy can be a way of balancing the changing needs and potential income gaps a client faces once they stop full-time work.

The funds released through an equity release plan are tax-free, regardless of whether a client chooses to release the funds in a lump sum, or as a series of smaller payments – and irrespective of how the money is spent.

Clients in the process of divorce

Divorce also carries difficult financial implications, particularly where a couple has shared a home over many years. Where an IFA has a client that is confronted with the loss of their home they may want to recommend equity release as a way forward.

Circumstances permitting, equity release can help a client undergoing divorce proceedings to meet the requirements of a divorce settlement, without needing to sell their residence. Indeed, an equity release plan could provide a relatively pain-free way of moving on from a challenging time in a client’s life.

Gifting and inheritance

Increasingly, equity release is being used by wealthier clients as a means to make outright gifts to children and grandchildren - a ‘living inheritance’ that ensures they see the benefits of their loved ones enjoying the money. This money is often being used as a deposit on a first home to help children not only afford the property they want but to get a much cheaper mortgage deal at the same time.

Clearly, equity release has a range of uses for high net worth clients whether it’s to enhance their retirement lifestyle, help them deal with marital or health changes or indeed to provide a ‘living inheritance’.

How do IFAs broach the subject of equity release with high net worth clients?

It’s our view that equity release should be included as part of a holistic approach to later life advice, and, for many high net worth clients, IFAs are well-placed to evaluate and explain the net benefits of equity release. By referring equity release clients to Key Partnerships, IFAs also stand to benefit from an average referral commission of £1,483* for each completed case, while simultaneously offering a smart financial move to a wealthy subset of their clients.

Do get in touch with us if you’ve any high net worth clients that have an oversized portion of their wealth locked up in property wealth – we’d love to help you add value to your financial advice proposition.

*Average referral payment for completed cases in 2018.

We use essential cookies to make our website work properly when you visit us. We’d also like your consent to set other non-essential cookies to help us improve our website and tailor the marketing you see.

Some cookies are optional, you can opt in or out of these cookies below.

Marketing cookies – These cookies help us tailor the advertisements you see on third party sites by understanding what interests you on our sites, such as the pages you view. We don’t combine this information with other personal information you provide us with.

Tracking cookies – These enable us to recognise repeat visitors to the site. By matching an anonymous, randomly generated identifier, we’re able to record specific browsing information such as how you arrive at the site, the pages you view, options you select, and the path you take through the site. By monitoring this information we’re able to make improvements to our sites.

Social cookies – These cookies allow you to share and like our pages through your favourite social network sites.